How Much Can You Actually Borrow for SLP Grad School Now?

New York University’s Speech@NYU program carries a total cost of $109,0561, far exceeding the new $50,000 annual federal loan cap.

Current Federal Borrowing Limits After the Ruling

The June 2026 court ruling temporarily preserves the higher professional-degree loan limit for speech-language pathology students4. That means SLP master’s candidates can currently borrow up to $50,000 per year in Direct Unsubsidized Loans, not the standard $20,500 graduate limit1. This is a critical distinction: without the ruling, most SLP students would be capped at $20,500 annually, leaving a much wider funding gap.

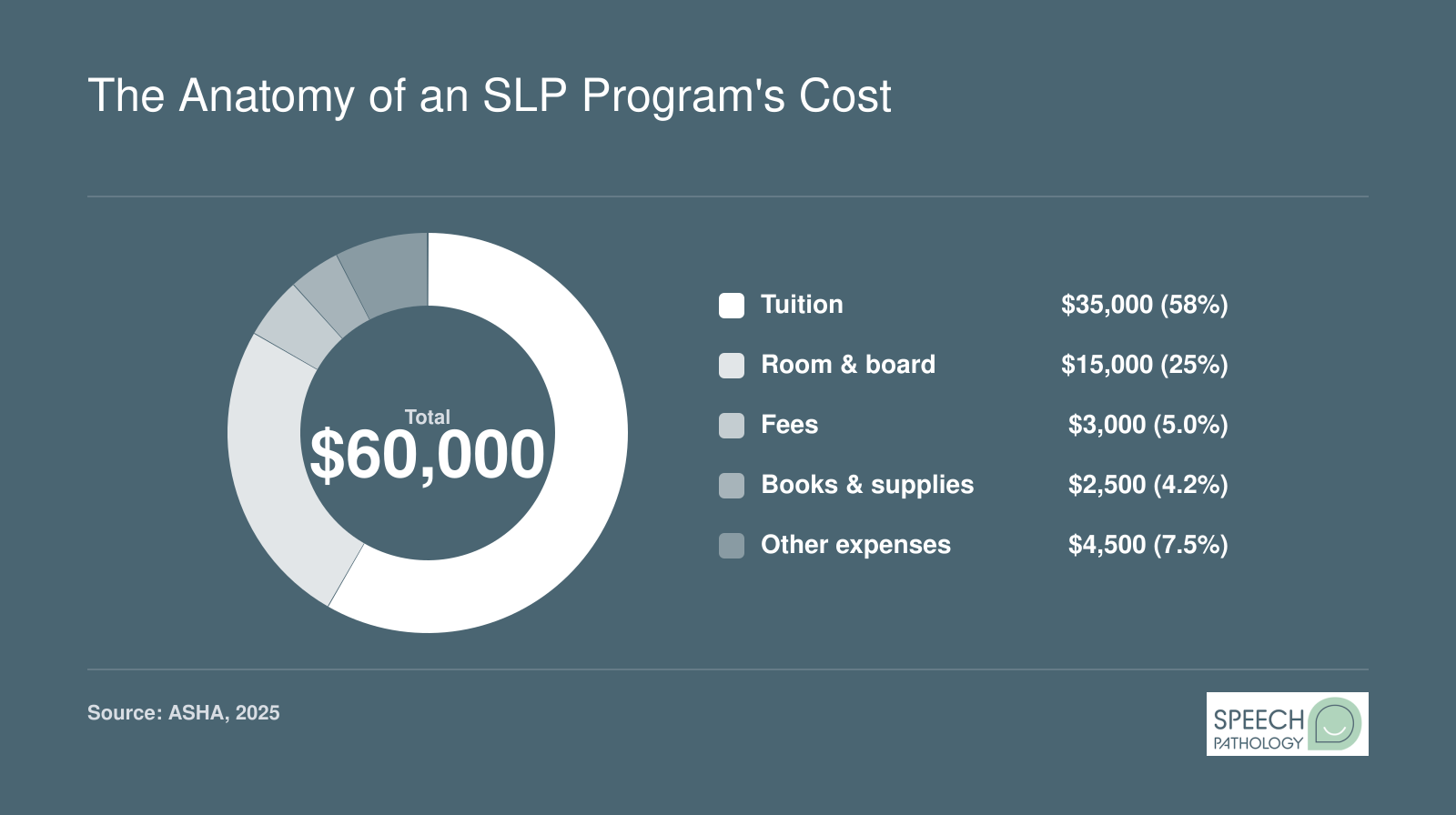

However, these are annual caps: the total you can borrow over your entire program depends on its length. For a typical two-year master’s, the total federal maximum would be $100,000. Remember, the Grad PLUS loan program is still being phased out, so these Direct Loan limits are your primary federal borrowing tool.

Cost Scenarios and Your Potential Funding Gap

Let’s compare actual 2026-2027 program costs (tuition, fees, and living expenses) to the $50,000 annual cap, assuming a two-year program and a $100,000 total federal loan ceiling:

- University of Pittsburgh (in-state): $30,894 total program cost2. No funding gap, federal loans can cover the full cost.

- University of Pittsburgh (out-of-state): $37,618 total program cost2. Also fully covered.

- University of Washington (resident EdSLP): $59,556 total program cost3. No gap.

- University of Washington (resident MedSLP): $75,376 total program cost3. No gap.

- University of Washington (nonresident EdSLP): $73,766 total program cost3. No gap.

- New York University (all students): $109,056 total program cost1. Expected gap of at least $9,056 after max federal loans.

These figures show that many public-university SLP programs fall well within the protected federal borrowing limit. High-cost private programs, however, can still leave you with a funding shortfall.

What Determines Your Actual Loan Amount

The $50,000 figure is a ceiling, not a guarantee. Your school’s financial aid office calculates your eligibility based on the cost of attendance (COA) minus any other financial aid. If your COA is $40,000 and you receive a $5,000 scholarship, you can only borrow up to $35,000 in federal loans, not the full $50,000. That’s why it’s essential to look at your own program’s COA, not just the borrowing limit.

Plan Ahead to Close the Gap

Calculate your total program cost (tuition, fees, books, living expenses) and subtract the maximum federal loans you can receive ($50,000 per year times your program’s length). If you see a gap, start exploring alternatives now: graduate assistantships, institutional scholarships, state loan-repayment programs, or private loans as a last resort. The earlier you identify the shortfall, the more time you have to secure funding, and the less stress you’ll face when the first tuition bill arrives.