How to Pay for SLP Grad School: Scholarships, Loans & More

A complete financial planning roadmap covering every funding source available to speech-language pathology graduate students.

By Benjamin Thompson, M.S., CCC‑SLPReviewed by SLP Editoral TeamUpdated July 27, 202624 min read

Points of interest…

In-state public SLP programs can cost as little as $6,000 total, while private programs may exceed $95,000.

The One Big Beautiful Bill Act changes Grad PLUS lending rules starting in 2026, directly affecting SLP borrowers.

PSLF, NHSC loan repayment, and TEACH Grants can eliminate tens of thousands in debt for SLPs in public service roles.

Layering federal loans with a graduate assistantship and a targeted scholarship consistently produces the lowest total debt at graduation.

An SLP master's degree typically costs between $40,000 and $120,000 or more, spread across two to three years of full-time study. That price tag creates a real financial planning challenge, especially when clinical placement hours limit your ability to work.

The good news: speech-language pathology students have access to a wider range of funding tools than most realize. Federal loans (with significant rule changes taking effect in 2026), SLP scholarships, graduate assistantships, loan forgiveness programs like PSLF and NHSC, and employer tuition reimbursement can all be combined into a layered strategy. The students who graduate with manageable debt are rarely relying on a single source. They are stacking three or four, and this guide walks you through every option.

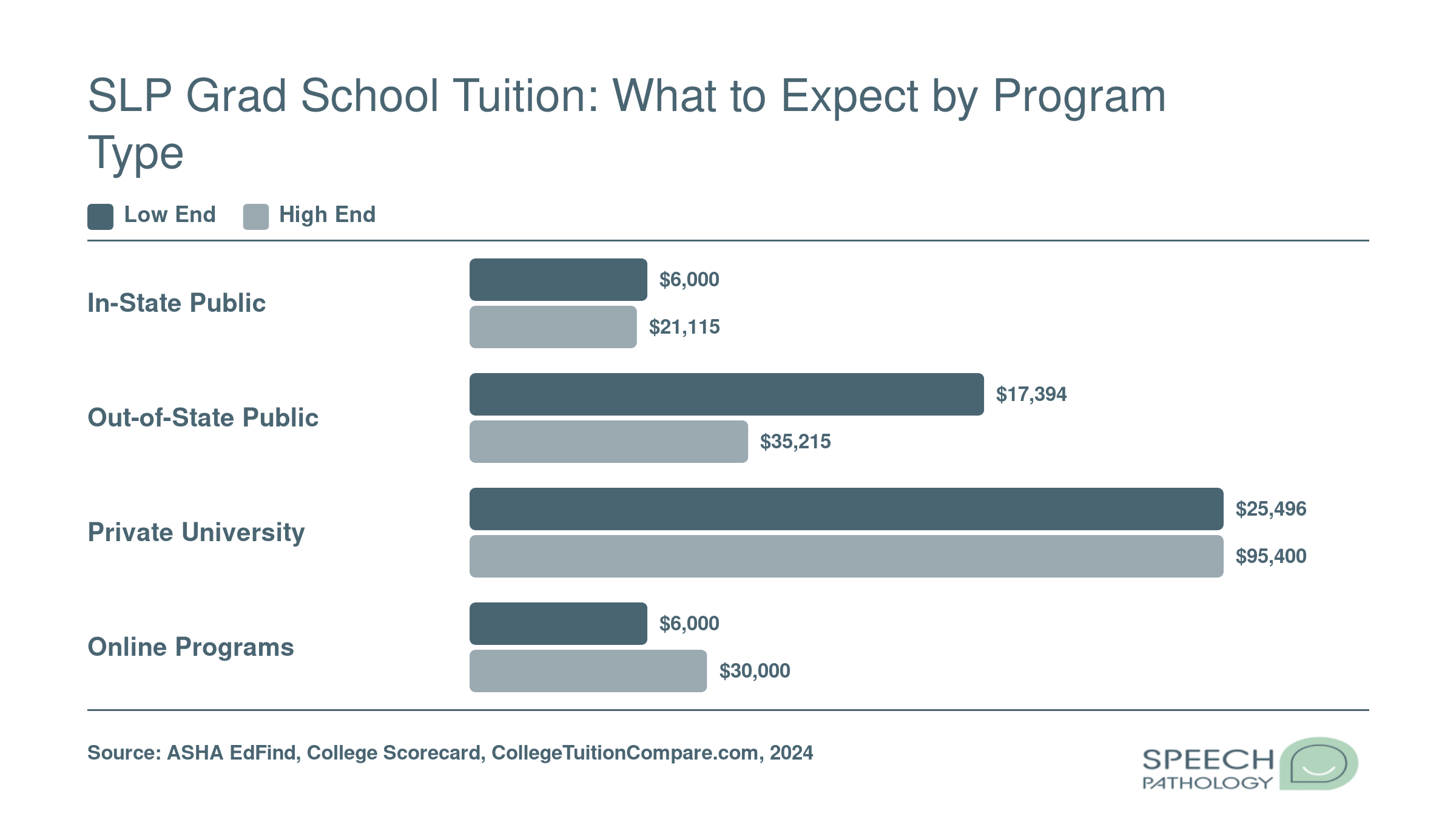

SLP Grad School Tuition: What to Expect by Program Type

SLP graduate tuition varies dramatically depending on the type of institution you attend. In-state public programs can cost as little as $6,000 for the full program, while private universities may top $95,000. Online programs add another layer of complexity, with per-credit rates that range widely and often ignore residency status altogether.

Federal Student Loans and the 2026 Grad PLUS Changes

If you are planning to start an SLP master's program in 2026 or later, a major shift in federal student lending will directly affect how you pay for school. The One Big Beautiful Bill Act, signed into law on July 4, 2025, eliminates the Federal Direct Grad PLUS Loan for new borrowers effective July 1, 2026.1 No replacement federal loan program has been created to fill the gap.2 Understanding what this means, and what you can do right now, is essential.

What Is Changing and Who Is Affected

Grad PLUS loans have historically allowed graduate students to borrow up to the full cost of attendance minus other financial aid, with no fixed dollar cap. That flexibility made them a lifeline for SLP students at programs where tuition and fees exceed what other federal loans cover. Starting July 1, 2026, students who have not already received a Grad PLUS disbursement will no longer be able to access this loan type at all.3

The only remaining federal borrowing option for graduate students will be the Direct Unsubsidized Loan, which carries an annual limit of $20,500 and an aggregate lifetime limit of $100,000 (including any undergraduate borrowing).4 For many SLP programs, especially out-of-state or private universities where total program costs can reach $80,000 to $120,000 or more, $20,500 per year will fall well short of what students need. The gap between available federal aid and actual tuition could be tens of thousands of dollars annually.

Legacy Borrower Provisions

There is a three-year transition window for students who are already enrolled. If you receive a Grad PLUS loan disbursement before July 1, 2026, and you remain continuously enrolled in your current program, you can continue borrowing through Grad PLUS until June 30, 2029.1 Legacy borrowers also retain access to Income-Based Repayment plans for their Grad PLUS balances.5 However, if you take a leave of absence or switch programs, you may lose that grandfathered eligibility. Students enrolled part-time should be aware that Direct Unsubsidized Loans may be prorated for less-than-full-time enrollment, further reducing available federal aid.4

Action Steps to Protect Your Funding

This is not a wait-and-see situation. Here are concrete steps to take now:

Apply and enroll before the cutoff if feasible: If you are on the fence about starting your SLP program in fall 2025 versus fall 2026, enrolling earlier could preserve your access to Grad PLUS loans for the duration of your degree.

Max out Direct Unsubsidized Loans first: Regardless of when you start, always borrow the full $20,500 annual allotment through Direct Unsubsidized Loans before turning to any other source. These carry lower interest rates and better borrower protections than private alternatives.

Start exploring alternatives now: With no federal replacement loan on the horizon, private education loans will become the primary option for many students who need to borrow beyond the unsubsidized cap.2 Begin researching lenders, comparing rates, and understanding the differences in repayment flexibility well before you need the money. We cover private loan considerations in detail later in this guide.

Contact your program's financial aid office: Every school is adjusting to these changes differently. Some may increase institutional aid, create new payment plans, or help you identify scholarships. Reach out to your financial aid advisor to understand how your specific program plans to support students through this transition.

The elimination of Grad PLUS loans makes every other funding source in your plan more important. SLP scholarships, assistantships, employer reimbursement, and careful budgeting are no longer just nice-to-haves. For many SLP students entering after July 2026, they will be essential pieces of a workable financial plan.

Scholarships and Grants for SLP Graduate Students

Scholarships are the closest thing to free money you will find, and speech-language pathology students have more options than many realize. The trick is knowing where to look, which awards match your profile, and when to apply. Below is a curated table of national scholarships, followed by tips for digging up lesser-known opportunities.

National Scholarships at a Glance

Scholarship

Sponsor

Amount

Typical Deadline

Type

Eligibility Highlights

Graduate Student Scholarship (General)

ASHA Foundation

$5,000

May 20, 2026

Merit-based

Full-time CSD grad students or accepted seniors; strong academics, three faculty recommendations

Graduate Student Scholarship for Minority Students

ASHA Foundation

$5,000

May 20, 2026

Diversity-focused

U.S. citizens from racial/ethnic minority groups in CSD graduate programs

Graduate Student Scholarship for International Students

ASHA Foundation

$5,000

May 20, 2026

Merit-based

Non-U.S. citizens enrolled in a U.S. CSD graduate program

NSSLHA Scholarship

ASHA Foundation

$5,000

May 20, 2026

Merit-based

Undergrad seniors with active National NSSLHA membership entering a CSD grad program

Dr. Lawrence D. Shriberg Memorial Scholarship

ASHA Foundation

$5,000

May 20, 2026

Research-focused

Grad students researching speech sound disorders, childhood apraxia, or genetic speech conditions

NBASLH Scholarships

National Black Assoc. for Speech-Language and Hearing

Varies

Varies (typically spring)

Diversity-focused

Students from underrepresented backgrounds pursuing CSD degrees

CAPCSD Doctoral Scholarships

CAPCSD

Varies

Varies

Merit/research

Doctoral-level CSD students; emphasis on future faculty development

EBS Healthcare Scholarship

EBS Healthcare

Varies

Varies (typically fall)

Merit-based

Graduate students in speech-language pathology or audiology

AAUW Selected Professions Fellowship

American Assoc. of University Women

Up to $20,000

Typically November

Need/merit, diversity-focused

Women in underrepresented fields, including CSD; U.S. citizens or permanent residents

Sertoma Communicative Disorders Scholarship

Sertoma International

$1,000

Typically March

Merit-based

Full-time grad students in CSD with a minimum 3.2 GPA

State Association Awards

Various state speech-language-hearing associations

$500 to $2,000+

Varies by state

Varies

Residency or enrollment in a program within the state; check your state association website

All ASHA Foundation scholarship details and deadlines are drawn from the current application cycle.1

Diversity, Need, and Merit: Matching Awards to Your Profile

If you are a student from a racial or ethnic minority group, the ASHA Foundation Minority Student Scholarship and NBASLH awards should be at the top of your list. Women pursuing CSD can tap the AAUW fellowship, which offers one of the largest single awards available to SLP students. For students driven primarily by research interests, the Shriberg Memorial Scholarship rewards a specific focus on speech sound disorders. Students considering a doctorate in speech pathology should also look at CAPCSD doctoral scholarships, which emphasize future faculty development. Everyone else should start with the ASHA Foundation General Scholarship and Sertoma, both of which rely on academic merit and do not restrict by demographic category.

Lesser-Known Opportunities Worth Pursuing

Beyond the major national awards, do not overlook two often-missed sources. First, your state speech-language-hearing association almost certainly offers at least one scholarship. These awards tend to draw fewer applicants, which improves your odds. Second, your university's graduate school and financial aid office may have department-specific or college-wide fellowships that never appear on national search engines.

Keep Your Search Current

Deadlines shift from year to year, new scholarships launch, and eligibility criteria change. Our SLP scholarships page is maintained as a living resource with updated deadlines and direct application links. Bookmark it early in your funding search so you never miss a window. Applying to even three or four scholarships per cycle can meaningfully reduce how much you borrow, and the time you invest now pays dividends for years after graduation.

Graduate Assistantships, Fellowships, and Fully Funded SLP Programs

Graduate assistantships and fellowships can dramatically reduce the cost of an SLP master's degree, sometimes eliminating tuition entirely. Understanding the differences between position types, and knowing how to pursue them strategically, can save you tens of thousands of dollars over two years.

Types of Funded Positions

Most SLP programs offer three categories of funded positions, each with different expectations and compensation structures:

Teaching assistantships (TAs): You assist a faculty member with undergraduate courses, grading, or lab supervision. TAs typically receive a partial or full tuition waiver plus a modest stipend.

Research assistantships (RAs): You work directly on a faculty member's funded research project, collecting data, running analyses, or managing study logistics. RAs often come with the most generous packages because they are tied to external grant funding, and they usually include a tuition waiver and stipend.

Clinical fellowships and practica assistantships: Some programs offer stipends for students who take on extra clinical responsibilities, such as running university clinic sessions or supervising undergraduate observation hours. These positions are less common and may provide a stipend only, without a tuition reduction.

Stipends for graduate assistantships in communication sciences and disorders generally range from about $10,000 to $20,000 per academic year. Most positions require 15 to 20 hours of work per week, which is a meaningful time commitment on top of a full course load.

The Scheduling Reality

One challenge worth planning for: assistantship hours can conflict with required clinical placements, especially during your second year when SLP externship schedules are less flexible. Some programs prioritize GA funding for first-year students and expect you to find external clinical placements (sometimes unpaid) in your second year. Ask department coordinators directly whether funding continues for both years and how scheduling conflicts are typically handled.

Are Fully Funded SLP Programs Realistic?

The phrase "fully funded SLP programs" appears frequently in online discussions, but at the master's level, truly fully funded offers are rare. Full funding packages that cover tuition, fees, a living stipend, and health insurance are far more common at the doctoral level, whether in a PhD in speech language pathology or SLP-D program. If you are committed to the master's path, your best strategy is to target programs with active, externally funded research labs. Faculty who hold grants from the National Institutes of Health, the Department of Education, or similar agencies often have line items in their budgets specifically designated for graduate student support.

How to Improve Your Chances

Funding is competitive, so a proactive approach matters:

Reach out to department graduate coordinators early, ideally before you submit your application, to ask about available assistantships and the application timeline.

Review faculty research pages and identify investigators whose work aligns with your interests. A brief, well-informed email expressing genuine interest in their lab can put you on their radar before funding decisions are made.

Ask specifically about second-year funding during program interviews. Some schools guarantee multi-year support while others allocate positions annually on a competitive basis.

Look beyond the department itself. University-wide fellowship competitions, diversity fellowships, and offices of graduate studies sometimes offer awards that SLP students overlook because they are not advertised within the program.

Combining a graduate assistantship with speech pathology financial aid and federal loans can build a strong funding stack that keeps borrowing to a minimum. Even a half-tuition waiver paired with a $12,000 stipend meaningfully changes your debt picture at graduation.

Questions to Ask Yourself

Have you maxed out federal Direct Unsubsidized Loans before considering private options?

Federal loans offer income-driven repayment plans and forgiveness eligibility that private lenders cannot match. Borrowing the full federal amount first protects your long-term flexibility, even if a private lender advertises a lower interest rate today.

Does your current or prospective employer offer tuition assistance for speech pathology coursework?

Hospitals, school districts, and rehabilitation companies increasingly cover partial tuition in exchange for a service commitment. Even a modest reimbursement of a few thousand dollars per year compounds across a two-year program and reduces total borrowing.

Have you contacted your program's department about second-year assistantship openings?

Many SLP programs reserve assistantships for continuing students, so positions that were not available at admission may open later. A graduate assistantship can include a tuition waiver plus a stipend, significantly lowering your out-of-pocket cost.

Are you eligible for forgiveness programs that could cut your effective cost by 30 to 50 percent?

Programs like Public Service Loan Forgiveness, the NHSC loan repayment program, and state-specific forgiveness options reward SLPs who work in schools, rural clinics, or nonprofit settings. Factoring potential forgiveness into your plan changes which loan types and repayment strategies make sense from day one.

Loan Forgiveness and Repayment Programs for SLPs

If you plan to work in a public school, hospital, nonprofit clinic, or university setting after graduation, you may be able to eliminate a significant portion of your student debt through federal and state repayment programs. Speech-language pathologists are well-positioned for several of these options because the profession naturally overlaps with qualifying employers and underserved communities.

Public Service Loan Forgiveness (PSLF)

PSLF remains the single most powerful debt-elimination tool for SLPs who work in the public or nonprofit sector. After making 120 qualifying monthly payments (roughly 10 years) under an income-driven repayment plan, the remaining federal loan balance is forgiven, tax-free. Whether you pursue a school SLP vs. medical SLP career, many common workplaces qualify as PSLF employers, including:

Public school districts: The largest employer category for SLPs, and virtually all are qualifying government employers.

Nonprofit hospitals and health systems: Many medical SLP positions fall under 501(c)(3) organizations.

University clinics and academic medical centers: Public universities and many private nonprofit institutions count.

State agencies and VA facilities: Government employers at any level automatically qualify.

The key is to enroll in an income-driven repayment plan as early as possible, certify your employer annually using the PSLF Help Tool, and keep careful records. Missing even one step can delay forgiveness.

TEACH Grants for School-Based SLPs

The TEACH Grant program offers up to $4,076 per year (with an aggregate limit near $16,000 for graduate students) to students who commit to working in high-need fields at low-income, Title I-eligible schools for at least four years after graduation. Speech-language pathology is designated as a high-need field, making SLP graduate students eligible.

There is one critical caveat: if you do not complete the four-year teaching service obligation within eight years of finishing your program, the entire grant converts into an unsubsidized federal loan with interest accruing from the original disbursement date. Before accepting a TEACH Grant, make sure you are genuinely committed to school-based practice in a qualifying setting.

NHSC and State Loan Repayment Programs

The National Health Service Corps (NHSC) Loan Repayment Program offers substantial awards (up to $75,000 for a two-year full-time commitment) to clinicians who serve in Health Professional Shortage Areas.2 However, the federal NHSC program currently limits eligibility to primary care, behavioral health, and oral health disciplines, which means SLPs do not qualify for the main federal NHSC program as of 2026.2

That said, the NHSC also funds State Loan Repayment Programs, and eligibility for these state-administered versions varies.3 Some states do include speech-language pathologists, so it is worth checking whether your state participates and which disciplines it covers. Contact your state's primary care office for the most current details.

Several states offer their own loan repayment or forgiveness programs that may be available to SLPs, depending on the specific eligibility criteria and settings involved:3

California State Loan Repayment Program: Awards up to $50,000 in exchange for a three-year service commitment in an underserved area. Eligibility for SLPs may depend on the specific shortage designation.

Texas programs: The state offers multiple options, including the Teach for Texas Loan Repayment Assistance Program (up to $20,000) and the Health Service Corps (up to $25,000), both targeting professionals who serve in high-need communities or schools.

New York programs: New York runs several repayment programs, including awards that can reach $90,000 or more for health professions faculty who commit to multi-year teaching obligations, as well as primary care service programs with awards up to $120,000 for four-year commitments. Eligibility criteria and qualifying disciplines vary by program.

These are just a few examples. Many other states operate similar initiatives, and program details change from year to year. Check your state's higher education authority or department of health website for the latest offerings. For a broader look at funding options, explore our SLP scholarships resource page.

Putting It All Together

Loan forgiveness and repayment programs reward you for doing work that many SLPs already find fulfilling: serving children in public schools, treating patients in underserved communities, or teaching the next generation of clinicians. The financial benefit can be enormous, potentially tens of thousands of dollars in forgiven debt. The tradeoff is that these programs require careful planning, consistent documentation, and a genuine commitment to qualifying service. Start researching your options now, well before you graduate, so you can align your career choices with the programs that offer the best return.

Private Loans and Employer Tuition Reimbursement

After you have maximized federal student loans, scholarships, and assistantships, you may still face a funding gap. Two additional tools can help close it: private student loans and employer tuition reimbursement. The comparison below highlights how federal Direct Unsubsidized Loans and private student loans differ across the dimensions that matter most to SLP graduate students. Below the table, you will find practical guidance on when private loans make sense, when they carry too much risk, and how to unlock tuition benefits from an employer.

Feature

Federal Direct Unsubsidized Loans

Private Student Loans

Interest Rate Type

Fixed rate set by Congress each year (currently 6.53% for graduate students in 2024-2025)

Fixed or variable rates depending on lender; variable rates may start lower but can rise significantly over the life of the loan

Borrower Protections

Built-in protections including deferment, forbearance, and discharge options in cases of disability or school closure

Protections vary by lender and are generally more limited; most private lenders offer fewer hardship options

Deferment and Forbearance

Automatic in-school deferment; multiple federal deferment and forbearance options after graduation

Some lenders offer in-school deferment, but post-graduation options are limited and lender-specific

Income-Driven Repayment (IDR) Eligibility

Eligible for all federal IDR plans, including the SAVE plan, which can cap payments at 10% of discretionary income

Not eligible for any federal income-driven repayment plan; repayment terms are set by the lender

Public Service Loan Forgiveness (PSLF) Eligibility

Fully eligible when repaid under a qualifying IDR plan while working for a nonprofit or government employer

Not eligible for PSLF under any circumstances

Credit and Cosigner Requirements

No credit check required (except for Grad PLUS loans); no cosigner needed

Approval and rate depend on credit score; a cosigner with strong credit can help secure a lower rate

Annual Borrowing Limit

Up to $20,500 per year in Direct Unsubsidized Loans (Grad PLUS can cover remaining cost of attendance)

Varies by lender, typically up to the full cost of attendance minus other aid received

Budgeting Tips and Cost-Of-Living Considerations

Tuition is only part of the equation. The total cost of attendance, which includes housing, food, transportation, health insurance, and supplies, often dwarfs the sticker price of a program. An SLP graduate student attending school in Manhattan or the San Francisco Bay Area can easily spend $15,000 to $25,000 more per year on living expenses than a peer in rural Kansas or small-town Mississippi. Before you commit to a program, build a realistic budget that captures every dollar you will spend over two or three years, not just the number on the tuition bill.

Calculate Your True Cost of Attendance

Start by researching the cost-of-living index for each city where you have been admitted. Factor in rent, groceries, utilities, and transit. Most universities publish an estimated cost of attendance that includes living expenses, but those figures often assume shared housing and modest spending. Cross-check them against local rental listings and grocery costs. If two programs charge similar tuition but sit in very different markets, the cheaper city could save you tens of thousands in total borrowing.

Practical Tactics to Lower Your Monthly Burn Rate

Small, consistent choices add up over a two-year program. A few strategies worth exploring:

Share housing near campus: Splitting a two-bedroom apartment with a fellow grad student can cut rent by 30 to 50 percent compared to living alone, and a shorter commute saves on gas or transit passes.

Compare student health insurance to marketplace plans: Many universities auto-enroll you in a campus plan. Before accepting it, compare premiums and coverage to Affordable Care Act marketplace options. In some states, marketplace subsidies make external plans significantly cheaper.

Tap departmental emergency funds: Most communication sciences and disorders departments maintain small emergency or professional-development funds that go underused simply because students never ask. These can cover unexpected costs like a broken laptop, conference travel, or clinical placement expenses.

Consider part-time or hybrid formats: If your program offers a part-time track, you can continue working while enrolled. This extends your time to degree, which delays your entry into full SLP earning potential, but it can dramatically reduce how much you need to borrow each semester.

The Part-Time Trade-Off

Choosing a part-time or hybrid program deserves honest consideration. Stretching a two-year degree into three or four years means you forgo one or two years of a full SLP salary, which currently averages around $89,000 nationally according to the Bureau of Labor Statistics. However, if the alternative is borrowing an additional $40,000 or more at graduate loan interest rates, the math can still work in your favor, especially if your employer offers tuition reimbursement while you study. Students who want to compress the timeline instead may want to explore accelerated SLP programs that shorten the path to the clinical fellowship.

Set Up Your Debt-to-Salary Gut Check

Before finalizing your program choice, take a few minutes to estimate your likely debt-to-starting-salary ratio. A common guideline across graduate fields is to keep total educational debt below your expected first-year salary. In the next section, we break down SLP salaries and debt loads by state so you can see which program locations offer the strongest return on investment. Running that calculation now, before you sign a promissory note, is one of the highest-value financial planning steps you can take.

SLP Salary Vs. Debt: Highest-Value States for New Graduates

Choosing where to practice after graduation can dramatically affect how quickly you pay off student loans. The table below shows the ten highest-paying states for speech-language pathologists based on Bureau of Labor Statistics (BLS) occupational data alongside estimated employment volume. Keep in mind that BLS median figures reflect all experience levels, so new graduates should focus on the 25th percentile column for a more realistic first-year earnings benchmark. When you weigh these salaries against typical SLP graduate debt loads of $50,000 to $100,000, states with strong entry-level pay and high employment demand offer the most favorable debt-to-income ratio. It is also worth noting that occupational therapists earn comparably in many of these states, but SLPs often have broader access to federal and state loan forgiveness programs because of the prevalence of school-based positions that qualify under programs like PSLF and TEACH Grants.

State

Median Annual Salary

25th Percentile Salary (Entry-Level Benchmark)

Estimated Employment

California

$99,730

$82,520

22,380

New York

$98,510

$79,920

16,540

New Jersey

$97,490

$80,150

6,680

Connecticut

$96,900

$79,680

3,380

Colorado

$95,850

$77,920

4,060

Massachusetts

$93,680

$76,530

7,380

Hawaii

$92,480

$76,020

900

Washington

$91,670

$76,250

5,600

Nevada

$90,830

$73,880

1,520

Alaska

$90,280

$75,290

580

Did You Know?

No single funding source will cover everything. The SLP graduate students who finish with the least debt consistently layer two or three strategies together: federal loans paired with a graduate assistantship or scholarship, followed by forgiveness-eligible employment after graduation. Think of your plan as a stack, not a single solution, and build each layer early.

Frequently Asked Questions About Paying for SLP Grad School

Financing an SLP master's degree involves a mix of strategies, and the best approach depends on your personal circumstances. Below are answers to some of the most common questions prospective and current graduate students ask about paying for speech pathology programs.

How do people normally pay for SLP grad school?

Most students use a combination of federal student loans, scholarships, graduate assistantships, and personal savings. Some also rely on employer tuition reimbursement or family support. The key is layering multiple funding sources so no single mechanism carries the full burden. Start by completing the FAFSA to unlock federal loan and grant eligibility, then apply for program-specific and external scholarships before considering private loans.

Can speech-language pathologists qualify for Public Service Loan Forgiveness?

Yes. SLPs who work full time for a qualifying employer, such as a public school district, nonprofit hospital, or government agency, can have their remaining federal loan balance forgiven after 120 qualifying payments under an income-driven repayment plan. The program is called Public Service Loan Forgiveness (PSLF). To stay on track, submit the Employment Certification Form annually and use the PSLF Help Tool on the Federal Student Aid website.

Do SLP graduate assistantships cover tuition?

Many do, but the specifics vary by university. A typical graduate assistantship provides a partial or full tuition waiver plus a modest monthly stipend in exchange for 10 to 20 hours of work per week. Duties may include assisting faculty with research, teaching undergraduate labs, or supporting clinic operations. Contact your program's department directly to ask about available positions and application deadlines.

Who gets paid more, OT or SLP?

Salaries for occupational therapists and speech-language pathologists are quite similar nationally. According to the Bureau of Labor Statistics, the median annual wage for SLPs was approximately $89,290 in 2023, while occupational therapists earned a median of about $96,370. Compensation varies significantly by setting, location, and experience, so the gap can narrow or reverse depending on where and how you practice.

How can I get my SLP master's degree paid for?

Pursuing a fully funded program with a graduate assistantship is one of the most effective routes. You can also apply for the TEACH Grant if you plan to work in a high-need school district, seek employer tuition reimbursement if you are already working in a healthcare or education setting, and stack external scholarships. Visit speechpathology.org's scholarships page for a curated list of awards available to SLP students.

Are there funding options for international SLP graduate students?

International students are generally ineligible for federal loans and most federal grants, but other options exist. Many universities offer merit-based scholarships, research assistantships, and teaching fellowships open to all admitted students regardless of citizenship. Some professional organizations and private foundations award grants to international students as well. Check with your program's financial aid office early, because application timelines for these awards can be months ahead of enrollment.